It’s time to take control of your pension planning.

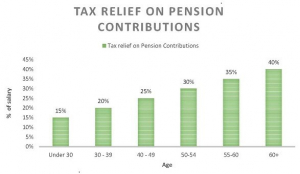

If you haven’t already started saving for retirement, it’s not too late. The current tax relief available within the pension framework was designed to allow older people save more money. As you can see from the table below, from age 50 the percentage of your salary on which tax relief is available, increases from 30% up to 40% by age 60. (This is capped at an earnings limit of €115,000).

If you have already started saving and have built up some level of retirement fund it is important to engage in the process so that you can take the necessary steps well in advance of your retirement age.

If you have already started saving and have built up some level of retirement fund it is important to engage in the process so that you can take the necessary steps well in advance of your retirement age.

Do you regularly read your benefit statement?

Irrespective of the type of pension arrangement that you have, you will be receiving an annual benefit statement. It is likely that up to now, these are something that received a quick glance and filed in a drawer to review in the future. This document not only sets out the value of your pension fund on an annual basis, but also some helpful illustrations of what the value of your fund will be at your retirement date. Knowing this allows you to keep doing what you have been doing with confidence or to make changes if necessary.

Irrespective of the type of pension arrangement that you have, you will be receiving an annual benefit statement. It is likely that up to now, these are something that received a quick glance and filed in a drawer to review in the future. This document not only sets out the value of your pension fund on an annual basis, but also some helpful illustrations of what the value of your fund will be at your retirement date. Knowing this allows you to keep doing what you have been doing with confidence or to make changes if necessary.

How are your retirement savings invested?

Your benefit statement will also tell you how your money is invested. You will usually have a choice in how your money is invested. This is known as your fund choice. The majority of people don’t deviate from their initial choice or the default provided over the course of their working life. It is with this in mind that many pension funds nowadays often have a Lifestyle strategy built into them as a default.

A Lifestyle strategy means that the fund in which you are invested in will automatically change its asset mix, on a gradual and regular basis as you move closer to your normal retirement age. Typically, these are structured to reduce the investment market risk in the run up to retirement. With many funds, the inbuilt Lifestyle strategy will take effect in the mid to late 50’s, for others it could be as early as age 50. It is important to know if this applies to your fund. It is also important to know if it fits in well with your post retirement plans. Which brings me to my final point.

What to do with your money at retirement?

There are different types of pension vehicles on the market and as such, there are different ways pensions are calculated at retirement. Knowing this will be an important factor in decisions you might have to make in advance of your retirement. If you are in a standard defined contribution company pension scheme, you will have the option of taking a tax-free lump sum and using the balance to buy either an annuity or investing in an Approved Retirement Fund (ARF).

There are different types of pension vehicles on the market and as such, there are different ways pensions are calculated at retirement. Knowing this will be an important factor in decisions you might have to make in advance of your retirement. If you are in a standard defined contribution company pension scheme, you will have the option of taking a tax-free lump sum and using the balance to buy either an annuity or investing in an Approved Retirement Fund (ARF).

More people than ever before are opting for the latter, but what are the differences? At a basic level, the annuity option is essentially taking the value of your retirement savings at your retirement date and giving them to a provider in return for a guaranteed income. The income that you will receive is dependent on your fund value, your age and health and potentially some other bells and whistles that can be added on.

On the other hand, the Approved Retirement Fund or ARF is keeping ownership of your fund and investing it further, while drawing an income from it throughout your retirement. There are advantages to both options and choosing the one that suits you is based on a range of individual factors.

However, having at least some idea of what you plan to do is important, particularly where your investment fund choice is concerned. If you are most likely planning to invest in an ARF, you should ensure that the fund in which your money is invested in the run up to retirement is not geared towards an Annuity.

Finally, you should be aware that if you are in your 50’s the State pension, which forms a substantial part of post retirement income for the majority of people in Ireland, is only available to you from age 68. If you are planning to retire earlier than that, this must be factored into your retirement plans. These small few steps can make all the difference to your income when you finally do retire.

Here to help you navigate your way to financial security.

The Milestone Advisory team are qualified financial services consultants. We specialise in helping professionals in the construction sector and related industries. Our team will work with you to review your finances, explaining your options in clear English.

No jargon – just the facts.

For further information please contact Susan O’Mara via email or phone: (01) 406 8020. Milestone Advisory DAC t/a Milestone Advisory is regulated by the Central Bank of Ireland.